A couple of years ago, my father turned 62 and casually asked me, "Do you think it's too late for me to buy life insurance?" I remember laughing a little, because in my head, term insurance was a "young person's product" — something you buy in your late 20s along with your first SIP and forget about for the next three decades.

Turns out, I was completely wrong. I spent the next few weeks calling insurers, reading policy wordings that felt like they were written to confuse me on purpose, and comparing quotes for term insurance for senior citizens. What I learned surprised me — and honestly, it changed how I think about my own insurance planning too.

If you're a business owner, a working professional nearing retirement, or someone helping a parent figure this out (like I was), this guide is for you. I'm going to walk you through everything I found — no jargon, no sales pitch, just what actually matters.

What Term Insurance for Senior Citizens Actually Means

Let's start simple. Term insurance is a pure protection plan. You pay a premium, and if something happens to you during the policy term, your family gets a lump sum (called the sum assured). There's no maturity benefit, no investment component — it's insurance in its most honest form.

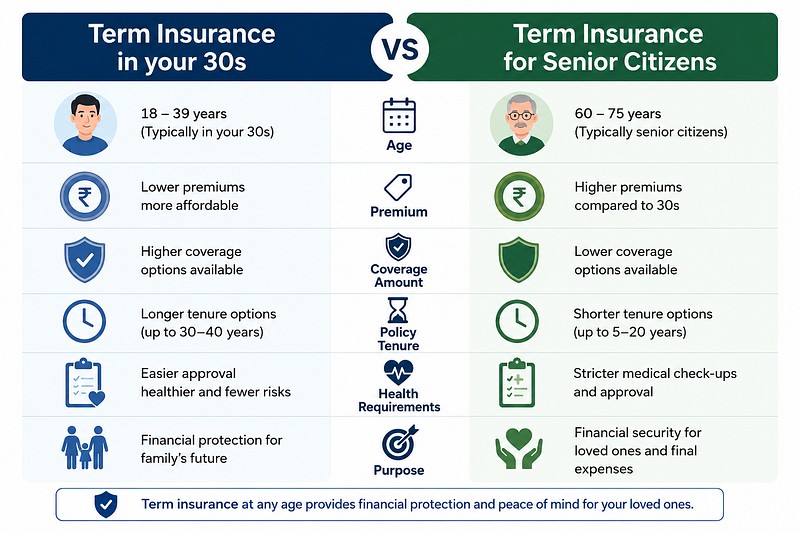

Term insurance for senior citizens is the same product, just designed — and priced — for people who are buying it later in life, typically after 55 or 60. The core idea doesn't change. What changes is the underwriting: insurers look more closely at your health, your income source (especially if you're retired), and they charge higher premiums because, statistically, the risk is higher at 60 than it is at 30.

I'll be honest — when I first started comparing term life insurance for senior citizens plans for my father, I assumed no insurer would touch a 62-year-old. That's not true anymore. The market has changed a lot over the last few years.

Is It Even Possible to Buy Term Insurance After 60?

Yes — and this is the part that surprised me most. A few years ago, most insurers capped entry age at 55 or 60. Today, several major insurers in India actively market term insurance plans for senior citizens, with entry ages stretching well beyond that.

Term Insurance for Senior Citizens Above 60 Years

Most insurers now allow entry between 55 and 65 years, with some going up to 70 or even 75 for specific plans. For example, insurers offering senior-focused products often position their entry window between 60 to 75 years, with flexible payout options designed for post-retirement needs. So if your parent — or you — is 61 or 63, you're very much within the eligible range for several plans.

Term Insurance for Senior Citizens Above 65 Years

This is where it gets a bit trickier, and I'll be upfront about it. Most insurers do not offer term insurance for a 70-year-old, and even for people who are 65, options start narrowing. That said, it's not impossible — some insurers do allow retired individuals aged 65 to 70 to purchase new policies, with coverage sometimes extending to age 85 or beyond. The catch is that these plans usually come with shorter policy terms, stricter medical underwriting, and noticeably higher premiums.

Here's the honest takeaway from everything I read and compared: if you're 58 or 60 and thinking "I'll buy it later, once I retire" — don't wait. The window doesn't close overnight, but it does get narrower and more expensive every year you delay. I actually recommended this to a client of mine (I do some financial content consulting on the side) who was 59 and hesitating. He bought his policy three months before turning 60, and it made a real difference to his premium.

How Much Does Term Insurance Cost for Senior Citizens in India?

Let's talk numbers, because this is usually the first question everyone asks.

Premiums for term insurance for senior citizens in India depend on a handful of factors: your age at entry, your health condition (especially diabetes, hypertension, or heart issues), your smoking habits, the sum assured you choose, and the policy term. Naturally, a 65-year-old will pay significantly more than a 45-year-old for the same cover — that's simply how risk-based pricing works in life insurance.

A few things that genuinely affect the premium you'll be quoted:

Your medical history matters more here than at any other life stage. When I got quotes for my father, the agent asked detailed questions about his sugar levels, blood pressure, and family medical history before even giving us a ballpark figure. Some insurers keep documentation minimal for seniors without pre-existing conditions, but if there's anything in your medical history, expect a full check-up requirement.

Your income proof matters too, especially post-retirement. Since term insurance is meant to replace income for your dependents, insurers want to see that you actually have an income stream — a pension, rental income, business income, or investment returns — to justify the sum assured you're applying for.

The policy term you choose also shifts the price a lot. Senior citizen term plans are often shorter in duration — think 5 to 20 years — because they're structured to align with the applicant's age and realistic life expectancy, rather than running for 30-40 years like a plan bought at 25 would.

If you want a realistic starting point, I'd suggest getting quotes from at least three insurers before deciding. Premiums for the same sum assured can vary quite a bit between companies for someone in the 60-65 age bracket, purely because each insurer prices senior-citizen risk differently.

What Actually Makes a Plan "The Best" — My Checklist

When people search for the best term insurance for senior citizens, I think they're often looking for a single "winner" plan. Honestly, that's not how I'd approach it, and it's not how I approached it for my father either. Instead, I built a checklist and compared plans against it. Here's what was on it.

Claim Settlement Ratio (CSR). This is non-negotiable for me. The CSR tells you what percentage of claims an insurer actually paid out in a given year. As per IRDAI's annual data, the industry-wide claim settlement ratio has consistently stayed above 98% in recent years, but individual insurers vary. I'd personally avoid any insurer with a CSR below 95% for at least the last three to five consecutive years — that consistency matters more than one great year. You can verify this directly on the IRDAI website rather than relying only on what an insurer's own marketing page tells you.

Entry and maturity age flexibility. Some plans that accept applicants at 60 only cover them till 75. Others extend maturity age up to 99 or 100. If your goal is legacy planning or making sure your spouse is covered for as long as possible, this matters a lot.

Payout flexibility. I didn't realize this until I started comparing plans, but several insurers now offer the option of a lump sum, a monthly income payout, or a mix of both for the death benefit. For a senior citizen's dependents — often a spouse who isn't used to managing a large lump sum — a staggered monthly payout can genuinely be more practical than one big number sitting in a bank account.

Riders that actually make sense at this age. Riders like critical illness cover or waiver of premium can add real value, but read the fine print — some riders have their own separate age caps that are lower than the base policy's.

Simplicity of the medical process. A few insurers offer minimal medical tests for seniors without prior health conditions, which speeds up the whole process considerably. If you're helping an elderly parent with limited mobility, this genuinely reduces the hassle.

For a deeper dive into how claim settlement ratios are calculated and why they matter across all life insurance products (not just senior plans), I'd recommend reading our detailed guide on www.mazaindia.com/claim-settlement-ratio-explained.

Insurers Offering Term Plans for Senior Citizens in India

Based on what I found while researching this for my own family, several established life insurers in India now have dedicated pages and products aimed at older applicants, including HDFC Life, Tata AIA, Axis Max Life, ICICI Prudential Life, Bajaj Allianz/Bajaj Finserv-linked plans, SBI Life, and LIC. Most of these insurers accept entry up to somewhere between 60-70 years, with maturity coverage extending as far as 99-100 years under whole-life-linked term variants.

I'm intentionally not ranking these into a "top 5" list here, because the right plan genuinely depends on your specific age, health profile, and what you're optimizing for — lower premium, higher maturity age, or flexible payouts. What I'd suggest instead: shortlist 3-4 insurers with strong, consistent CSRs, request quotes for the same sum assured and term, and compare like-for-like. That's exactly what I did before we finalized my father's policy.

If you want help figuring out how much cover you actually need before you start comparing insurers, we've written a separate breakdown here: www.mazaindia.com/how-much-term-insurance-cover-do-i-need.

Tax Benefits on Term Insurance for Senior Citizens

Here's something a lot of people miss, especially if they've been away from active tax filing since retirement: term insurance premiums still come with tax benefits, though the rules have recently been renumbered.

From April 1, 2026, India's new Income Tax Act, 2025 has restructured the old familiar sections. The erstwhile Section 80C is now Section 123, and it allows individuals and Hindu Undivided Families to claim a deduction of up to S77;1,50,000 per tax year on eligible investments listed under Schedule XV, which includes life insurance premiums. This benefit continues to apply only if you choose the old tax regime — it isn't available under the new default regime.

If your term plan includes health-related riders, such as a critical illness benefit, that portion may qualify separately. Under the new Act, this falls under Section 126, which allows deductions on health-related premiums up to S77;25,000, with a higher limit of S77;50,000 for senior citizens.

And on the payout side — the good news for your family — the death benefit your nominee receives from a term plan continues to be tax-exempt under Section 11, read with Schedule II of the Income Tax Act, 2025 (this replaces what used to be known as Section 10(10D)), subject to the usual conditions.

I'd genuinely recommend talking to a tax advisor before you file, especially if you're managing this transition from the old section numbers to the new ones for the first time. Tax rules change, and what applies this year might get tweaked in the next budget.

Common Mistakes I Noticed Business Owners and Professionals Make

Since I work closely with professionals and small business owners through my content work, I've noticed a pattern in how people approach this topic — and a few mistakes come up again and again.

The biggest one is treating term insurance as something that becomes "irrelevant" after retirement. I get the logic — if your kids are settled and the home loan is paid off, why do you need life cover? But here's the thing: if you still have a spouse who depends on your pension, or you're a business owner whose absence would create a financial gap for the business or co-owners, term insurance isn't irrelevant at all. It becomes income replacement and legacy protection rolled into one.

The second mistake is waiting for the "right time" that never comes. I've seen this with clients in their late 50s who kept postponing the decision, only to find that by 63, their options had narrowed and premiums had jumped. Age is the one variable in this entire equation that only moves in one direction.

The third mistake — and I made a version of this myself — is not disclosing medical history accurately to save on premium. Insurers do detailed underwriting, and if something is discovered later that wasn't disclosed, it can lead to a claim being rejected, which defeats the entire purpose of buying the policy in the first place. It's simply not worth the risk.

My Step-by-Step Approach to Buying One

If I were doing this again today, here's exactly how I'd go about it, based on what worked when I did this for my father:

I'd start by calculating the actual cover needed — not a random round number, but something based on existing liabilities, dependents' needs, and any income replacement required for a spouse. Then I'd shortlist insurers based on consistent claim settlement ratios over the last several years, not just the most recent one. After that, I'd request quotes for the same sum assured, same term, and same riders across at least three insurers, so the comparison is genuinely apples-to-apples. Before signing anything, I'd read the exclusions section closely — this is the part everyone skips, and it's where the real details live. Finally, I'd keep all medical disclosures completely honest, because that's what protects your family's claim later, not what saves you a few thousand rupees in premium today.

It took me about three weeks from start to finish, most of which was comparing quotes and getting my father through the medical tests. In hindsight, it was a manageable process — just one that required patience and a fair bit of homework.

Frequently Asked Questions

Can a 65-year-old still buy term insurance in India? Yes, though options are more limited than at 60. Some insurers extend entry up to 65-70 years, but expect a shorter policy term, mandatory medical tests, and a higher premium.

Is term insurance for senior citizens worth the cost? If you have dependents relying on your income or pension, or liabilities that would fall on your family, it's generally worth considering — even at a higher premium — because the alternative is leaving that financial gap uncovered.

Do senior citizens need to undergo medical tests for term insurance? In most cases, yes. Some insurers offer relaxed or minimal checks for applicants without pre-existing conditions and lower sum assured requests, but a basic health assessment is standard.

What documents are required to buy term insurance for senior citizens in India? Typically, identity proof, address proof, age proof, recent photographs, income proof (like pension slips or bank statements), and medical reports.

Are NRIs above 60 eligible to buy term insurance in India? Yes, many insurers allow NRIs above 60 to apply, provided they submit the required documentation, including proof of Indian citizenship or origin and residency abroad.

Final Thoughts

Buying term insurance for senior citizens isn't as complicated — or as impossible — as it might seem at first. The market has genuinely opened up over the last few years, and there are real, credible options available even if you're 62, 65, or in some cases older. What matters most is starting the process early, comparing plans honestly, and being transparent about your health when you apply.

If my father's experience taught me anything, it's this: the "right time" to buy term insurance as a senior citizen is almost always now, not later. Every year you wait narrows your options and raises your premium — and that's a cost that only grows with time.

For more on getting your broader retirement and income-protection planning in order, you might also want to read our related guide on www.mazaindia.com/retirement-planning-for-senior-citizens-india.

This article is for general informational purposes only and does not constitute financial or insurance advice. Please verify current entry ages, premiums, tax provisions, and claim settlement ratios directly with insurers or on the IRDAI website before making a purchase decision, and consult a qualified financial or tax advisor for guidance specific to your situation.