Let me start with a confession. When I first started freelancing, I thought insurance was something only "real" companies needed — the kind with offices and employees and a logo on a building somewhere. I was wrong, and I learned it the expensive way.

A client once threatened to sue me over a missed deadline that (according to them) cost their business money. Nothing came of it in the end, but the three sleepless nights I spent Googling "what happens if I get sued as a freelancer" taught me more about small business insurance than any textbook ever could. That scare is the reason I now treat insurance the same way I treat a smoke detector — you hope you never need it, but you really don't want to find out what happens without one.

If you're a business owner, a freelancer, a student thinking about starting something on the side, or just someone trying to understand insurance for small business owners, this guide is written for you. No jargon-heavy insurance-speak. Just a plain, human breakdown of what matters.

Why Small Business Insurance Isn't Just an "Extra Expense"

Here's the thing that took me way too long to understand: insurance isn't really about protecting against bad luck. It's about protecting your ability to keep operating after something goes wrong.

A story that stuck with me involves an independent summer camp. Two instructors working there had their own professional liability insurance. When a student got injured on their watch, the insurance paid out the settlements, and both instructors were able to move on with their careers relatively unscathed. But the camp owner, who didn't have adequate liability coverage, ended up tangled in litigation for over two decades. Two decades. That's not a typo — it drained the owner's time, money, and honestly, their peace of mind.

That single comparison tells you everything about why liability insurance for small business matters so much. A business might comfortably handle a million dollars in expenses spread out across years of operations. What it usually can't survive is a single, sudden million-dollar lawsuit. Insurance basically spreads that catastrophic risk into predictable monthly payments — and it also covers legal defense costs, even when a claim against you is completely baseless.

The Core Policies Every Business Owner Should Actually Understand

I'm not going to throw fifteen insurance types at you and expect it to make sense. Let's go through the ones that actually matter, one at a time, the way I'd explain it to a friend over coffee.

General Liability Insurance (the foundation)

General liability insurance for small business — sometimes called Public Liability insurance outside the US — is the one policy almost every business needs. Think of it as covering the "oops" moments: a customer slips on a wet floor, a courier trips over your equipment, or an employee accidentally spills coffee on a client's laptop.

It also covers what's called "personal and advertising injury" — things like accidental libel, slander, or even a copyright slip-up in a marketing campaign. What it won't cover is your own employees getting hurt (that's a different policy, more on that below), damage to your own property, or anything intentional or illegal.

Professional Liability (Errors & Omissions)

If you give advice or provide a service for a living — consulting, accounting, design, coding, real estate — this one's for you. Professional liability insurance, also called E&O coverage, protects you if a client claims your negligence or a mistake cost them money.

Picture an accountant who makes a clerical error that triggers a client's tax penalty, or a software firm that misses a contractual deadline and costs the client revenue. This is the policy that steps in for those situations. It's basically a non-negotiable for consultants, lawyers, and tech freelancers.

Commercial Property and Business Interruption

This one covers your physical stuff — your office, equipment, inventory, signage — against fire, theft, storms, and vandalism. Paired with it is Business Interruption insurance, which replaces lost income and covers fixed costs like rent and payroll if a covered event forces you to shut down temporarily. Without this, a fire doesn't just damage your building — it can quietly bankrupt you while you're rebuilding.

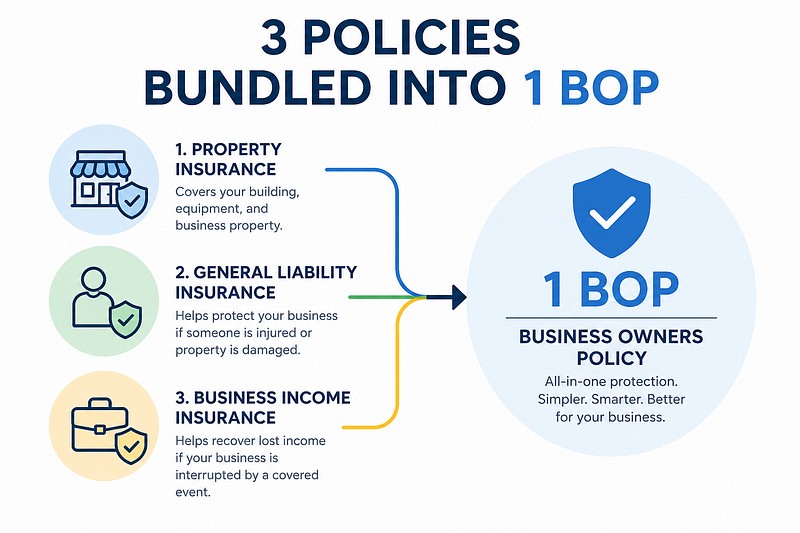

The Business Owner's Policy (BOP): The Smart Shortcut

Here's a tip that saved me money when I finally set up proper coverage: instead of buying General Liability, Commercial Property, and Business Interruption separately, most small businesses can bundle them into a single Business Owner's Policy (BOP). It's usually cheaper than buying each one individually, and it's built specifically for companies with under 100 employees and revenue under $5 million.

Cyber Liability Insurance

If you store any customer data — even just email addresses — you're a target. Cyber liability insurance covers the costs of a data breach: forensic investigation, legal counsel, customer notification, PR, credit monitoring, and sometimes even ransomware payouts. This isn't just for tech companies anymore; even a small retail shop with an online store needs to think about this.

Commercial Auto and Umbrella Insurance

Personal auto insurance almost always excludes business use — this is called a "livery exclusion." If you or your employees drive for work, you need Commercial Auto coverage, full stop.

Umbrella insurance, meanwhile, is your backstop. If a lawsuit exceeds your primary policy's limit, umbrella coverage kicks in to cover the rest. I think of it as a safety net under the safety net.

Protecting Your People: Workers' Comp and Health Coverage

If you have even one employee, in most places you're legally required to carry Workers' Compensation insurance. It covers medical costs, partial wage replacement, and disability benefits after a workplace injury — and in exchange, it shields you from direct negligence lawsuits from employees.

When it comes to health coverage, small business owners in the US typically choose between HMO, PPO, EPO, and POS plans:

| Plan Type |

Network Flexibility |

Referral Needed |

Avg. Annual Cost |

| HMO |

In-network only |

Yes |

~$8,285 |

| PPO |

High flexibility |

No |

~$9,119 |

| EPO |

In-network only |

No |

Variable |

| POS |

Out-of-network allowed |

Yes |

~$8,316 |

If you're a US-based small business with fewer than 25 full-time employees and average salaries around $56,000 or less, it's worth looking into the Small Business Health Options Program (SHOP) tax credit — it can meaningfully offset your costs if you contribute at least half of employee premiums.

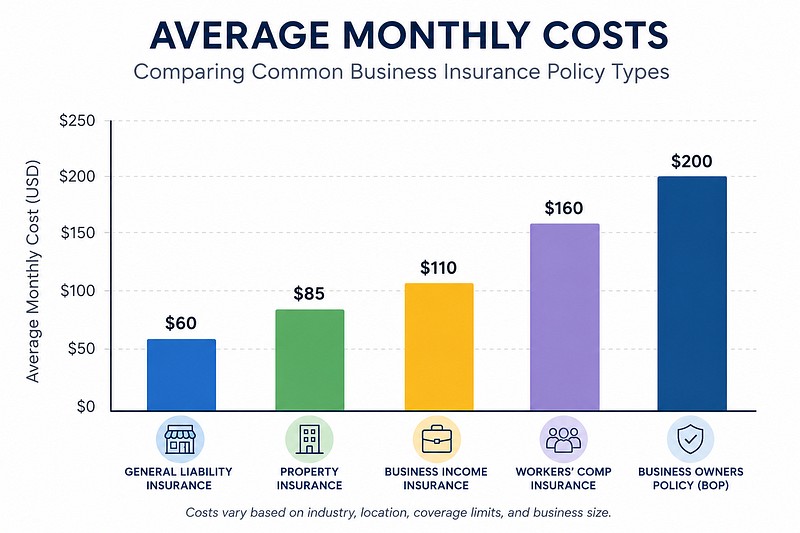

What Does Small Business Insurance Actually Cost?

This is the question everyone actually wants answered, so let's not dance around it. Small business insurance cost depends heavily on your industry, payroll, location, and claims history — but here are rough US monthly averages to give you a starting point:

- General Liability: around $45/month

- Workers' Compensation: around $54/month

- Professional Liability (E&O): $61–$88/month

- Business Owner's Policy (BOP): $57–$83/month

- Commercial Property: $67–$108/month

- Cyber Liability: $129–$145/month

- Commercial Auto: $138–$245/month

If you're in India, the numbers naturally look different. A Commercial General Liability policy typically runs S77;50,000–S77;1,50,000 annually for around S77;7.5 crore in coverage, while Professional Indemnity for IT/tech firms can run S77;1,25,000–S77;2,00,000 given the global exposure involved. Insurers like ICICI Lombard and HDFC Ergo have built modular products specifically for the MSME segment, letting you pick only the coverages you actually need instead of paying for a generic bundle.

One thing that actually helped me get a more accurate small business insurance quote was being precise about my job classification. A contractor forum thread I read once made a great point — a handyman doing carpentry pays very differently than one doing plumbing, because plumbing carries a much higher risk of water damage claims. Being vague about what you actually do tends to push your quote higher, not lower.

Industry-Specific Coverage: One Size Doesn't Fit All

If you run a restaurant, you'll likely need Liquor Liability (if you serve alcohol), Food Contamination coverage for spoilage during power outages, and Food Poisoning liability extensions.

If you're in e-commerce or sell physical products, Product Liability insurance is essential — a fairly standard benchmark is $1 million per occurrence with $2 million aggregate, usually costing $20–$100/month depending on your product category.

If you're in construction or handyman work, you'll want Operations and Completed Operations Liability (covering issues that show up after the job's done), Tools and Equipment coverage, and Builders Risk insurance for materials during active construction.

For a deeper breakdown by profession, check out our guide on insurance for freelancers and consultants

Where Claims Actually Go Wrong

I think this is the most underrated part of the whole insurance conversation — nobody talks about how claims actually get denied.

One recurring pattern: gig economy drivers using personal vehicles for deliveries or rideshare without commercial coverage. The moment a vehicle is used to transport goods or people for a fee, personal auto insurance's "livery exclusion" kicks in, and claims get denied outright.

Another pattern involves non-cooperation. If an at-fault party refuses to communicate with their own insurer, that insurer can eventually deny the claim due to non-cooperation — leaving the victim to file through their own policy and let subrogation sort it out later.

And then there's the obvious one: illegal activity voids coverage. There's a documented case of a hotel owner filing a business interruption claim over "noxious odors" driving customers away — only for adjusters to discover a meth lab operating in a room on the property. Claim denied, building condemned.

The lesson across all of these: read your exclusions carefully, keep your policy type matched to your actual business activity, and always cooperate with your insurer's investigation.

Occurrence vs. Claims-Made: A Detail That Trips People Up

This one's subtle but important. General Liability policies are usually "occurrence" based — they cover incidents that happened during the policy period, no matter when the lawsuit is actually filed. Professional Liability and D&O policies, on the other hand, are usually "claims-made" — meaning both the incident and the claim need to happen while the policy is active.

If you cancel a claims-made policy, you lose coverage for past work unless you buy what's called "tail coverage" — an extended reporting period. This is easy to miss, and it's exactly the kind of detail that catches people off guard when they switch insurers.

How to Actually Choose the Best Small Business Insurance

When people ask me how to find the best small business insurance, my answer is always: don't just chase the cheapest quote. Look at three things — financial strength, complaint history, and how well the coverage actually fits your industry.

For financial strength, AM Best ratings are the gold standard. An "A" or higher rating tells you the insurer can actually pay out claims during a bad year, not just a good one. You can also check the National Association of Insurance Commissioners (NAIC) database to see how many complaints an insurer has racked up relative to its size — a genuinely useful, often-overlooked step before signing anything. You can check that directly at naic.org

In the US market, names like The Hartford, Chubb, and NEXT Insurance consistently show up with strong ratings and low complaint levels. NEXT in particular is worth mentioning if you want speed — it's a fully digital insurer that can generate a certificate of insurance in minutes, which is genuinely useful if a client needs proof of coverage on short notice.

In India, ICICI Lombard and HDFC Ergo dominate the MSME space, with ICICI Lombard notably capable of settling small claims (up to S77;5 lakh) within about ten days through a virtual survey process — a big deal if you've ever dealt with the alternative of weeks-long claim delays.

A Few Things I'd Tell My Past Self

If I were starting over, here's what I'd do differently from day one:

Get a quote before you think you need one. Waiting until after a scare (like mine) means you're shopping for insurance while stressed, which rarely leads to good decisions.

Bundle where it makes sense. A BOP saved me more than I expected compared to buying policies separately.

Read your exclusions, not just your coverage. The exclusions are where claims actually get denied — that's where the real information is.

Match your policy to what you actually do. Being vague on your application to "save money" almost always backfires later.

If you're just getting started and want a simpler starting point, our piece on business insurance walks through the bare minimum coverage most new businesses should have on day one.

Final Thoughts

Insurance will never feel exciting to buy. Nobody wakes up thrilled to compare quotes for small business liability insurance. But the difference between a business that survives a bad year and one that doesn't often comes down to a policy nobody thought much about until they desperately needed it.

Treat it the way I eventually learned to — not as a cost, but as the thing standing between a bad day and the end of your business.